Fractional-reserve banking

| Banking | |

|

Types of banks |

|

|

Deposit accounts |

|

|

ATM card |

|

|

Electronic funds transfer |

|

|

Banking terms |

|

|

List of banks |

|

|

Finance series |

|

| Finance |

|---|

|

Financial markets

Bond market

Stock market (equity market) |

|

Financial instruments

Cash:

Deposit |

|

Structured finance

Capital budgeting |

|

Personal finance

Credit and debt

Student financial aid |

|

Government spending:

Transfer payment |

|

|

|

Financial regulation

Finance designations

Accounting scandals |

|

Standards

ISO 31000

International Financial Reporting |

|

Economic history

Stock market bubble

Recession |

Fractional-reserve banking is the banking practice in which banks keep only a fraction of their deposits in reserve (as cash and other highly liquid assets) and create the remainder as 'cheque book money', while maintaining the simultaneous obligation to redeem all these deposits upon demand.[1][2] Fractional reserve banking necessarily occurs when banks lend out funds that it does not have on deposit instead of funds solely received from deposit accounts, and is practiced by all modern commercial banks.

The practice of fractional reserve banking expands the money supply (cash and demand deposits) beyond what it would otherwise be. Due to the prevalence of fractional reserve banking, the broad money supply of most countries is a multiple larger than the amount of base money created by the country's central bank. That multiple (called the money multiplier) is determined by the reserve requirement or other financial ratio requirements imposed by financial regulators, and by the excess reserves kept by commercial banks.

Central banks generally mandate reserve requirements that require banks to keep a minimum fraction of their demand deposits as cash reserves. This both limits the amount of money creation that occurs in the commercial banking system, and ensures that banks have enough ready cash to meet normal demand for withdrawals. Problems can arise, however, when a large number of depositors seek withdrawal of their deposits; this can cause a bank run or, when problems are extreme and widespread, a systemic crisis. To mitigate these problems, central banks generally regulate and oversee commercial banks, act as lender of last resort to commercial banks, and also insure the deposits of the commercial banks' customers.

Contents |

History

Prior to the 1800s, savers looking to keep their valuables in safekeeping depositories deposited gold coins and silver coins at goldsmiths, receiving in turn a note for their deposit (see Bank of Amsterdam). Once these notes became a trusted medium of exchange an early form of paper money was born, in the form of the goldsmiths' notes.[3]

As the notes were used directly in trade, the goldsmiths observed that people would not usually redeem all their notes at the same time, and they saw the opportunity to invest their coin reserves in interest-bearing loans and bills. This generated income for the goldsmiths but left them with more notes on issue than reserves with which to pay them. A process was started that altered the role of the goldsmiths from passive guardians of bullion, charging fees for safe storage, to interest-paying and interest-earning banks. Thus fractional-reserve banking was born.

However, if creditors (note holders of gold originally deposited) lost faith in the ability of a bank to redeem (pay) their notes, many would try to redeem their notes at the same time. If in response a bank could not raise enough funds by calling in loans or selling bills, it either went into insolvency or defaulted on its notes. Such a situation is called a bank run and caused the demise of many early banks.[3]

Repeated bank failures and financial crises led to the creation of central banks – public (government) or privately owned institutions that with the authority of enacted national/federal statutes oversee and regulate commercial banks, impose reserve requirements, and act as lender-of-last-resort if a bank is low on liquidity. The emergence of central banks mitigated the dangers associated with fractional reserve banking.[4][5]

Reason for existence

The United States' Federal Reserve asserts that fractional reserve banking provides benefits to the economy and the banking system:[6]

The fact that banks are required to keep on hand only a fraction of the funds deposited with them is a function of the banking business. Banks borrow funds from their depositors (those with savings) and in turn lend those funds to the banks’ borrowers (those in need of funds). Banks make money by charging borrowers more for a loan (a higher percentage interest rate) than is paid to depositors for use of their money. If banks did not lend out their available funds after meeting their reserve requirements, depositors might have to pay banks to provide safekeeping services for their money. For the economy and the banking system as a whole, the practice of keeping only a fraction of deposits on hand has an important cumulative effect. Referred to as the fractional reserve system, it permits the banking system to create money.

Thus fractional reserve banking is a consequence of modern bank lending: a bank has cash reserves that cover only a fraction of deposits when it lends some of those deposits out. The fractional reserve system allows banks to act as financial intermediaries — facilitating the movement of funds from savers to investors in a society.[5][7]

Small savers often cannot lend or invest their meager savings, for want of knowledge and sufficient capital to make a loan. Likewise, without financial intermediaries, borrowers must seek out someone who can loan them the exact amount they need, instead of being able to draw on several loans from different small savers. Savers also face significant risk as individual investors, since if they lend to a single firm or individual, that entity can collapse, leaving the saver penniless. Furthermore, if they act as individual lenders, savers must wait for their loans to mature before recouping their money; a bank can make their deposits available at any time. Banks have the advantage of significant economies of scale when making investment and lending decisions, as they have access to knowledge and expertise which individual investors or lenders generally do not. Without fractional-reserve banking, a great deal of money would sit "idle", as savers stored up their money, while entrepreneurs went without the capital they seek.[8]

According to mainstream economic theory, regulated fractional-reserve banking also benefits the economy by providing regulators with powerful tools for manipulating the money supply and interest rates, which many see as essential to a healthy economy.[9] Moreover, the existence of fractional-reserve banking allows either the central bank or individual banks (under a free banking regime) to create money virtually at will, allowing the supply of money to adjust to changing demand for money. A full-reserve banking system with a fixed money supply would result in deflation as the economy grows. However, this deflation is likely to have deleterious consequences if some prices are stickier than others; in particular, wages are often significantly stickier than other prices. Most economists believe that given wage stickiness, the adjustment costs of deflation are significantly higher than an equivalent inflation. As such, mainstream economic thinking prefers the inflation brought about by fractional-reserve banking to the necessary deflation of a full-reserve banking policy regime.[10]

Member banks which fall under the umbrella of the main central bank benefit from different bankruptcy regulation than a typical business. For this reason the demand deposits of most banks will retain their value in spite of circumstances which would otherwise jeopardize their credit-worthiness.

How it works

The nature of modern banking is such that the cash reserves at the bank available to repay demand deposits need only be a fraction of the demand deposits owed to depositors. In most legal systems, a demand deposit at a bank (e.g. a checking or savings account) is considered a loan to the bank (instead of a bailment) repayable on demand, that the bank can use to finance its investments in loans and interest bearing securities. Banks make a profit based on the difference between the interest they charge on the loans they make, and the interest they pay to their depositors. Since a bank lends out most of the money deposited, keeping only a fraction of the total as reserves, it necessarily has less money than the account balances of its depositors.

The main reason customers deposit funds at a bank is to store savings in the form of a demand claim on the bank. Depositors still have a claim to full repayment of their funds on demand even though most of the funds have already been invested by the bank in interest bearing loans and securities.[11] Holders of demand deposits can withdraw all of their deposits at any time. If all the depositors of a bank did so at the same time a bank run would occur, and the bank would likely collapse. Due to the practice of central banking, this is a rare event today, as central banks usually guarantee the deposits at commercial banks, and act as lender of last resort when there is a run on a bank. However, there have been some recent bank runs: the Northern Rock crisis of 2007 in the United Kingdom is an example. The collapse of Washington Mutual bank in September 2008, the largest bank failure in history, was preceded by a "silent run" on the bank, where depositors removed vast sums of money from the bank through electronic transfer. However, in these cases, the banks proved to have been insolvent at the time of the run. Thus, these bank runs merely precipitated failures that were inevitable in any case.

In the absence of crises that trigger bank runs, fractional-reserve banking usually functions smoothly because at any one time relatively few depositors will make cash withdrawals simultaneously compared to the total amount on deposit, and a cash reserve can be maintained as a buffer to deal with the normal cash demands from depositors seeking withdrawals. In addition, in a normal economic environment, cash is steadily being introduced into the economy by the central bank, and new funds are steadily being deposited into the commercial banks.

However, if a bank is experiencing a financial crisis, and net redemption demands are unusually large over a period of time, the bank will run low on cash reserves and will be forced to raise additional funds to avoid running out of reserves and defaulting on its obligations. A bank can raise funds from additional borrowings (e.g. by borrowing from the money market or using lines of credit held with other banks), or by selling assets, or by calling in short-term loans. If creditors are afraid that the bank is running out of cash or is insolvent, they have an incentive to redeem their deposits as soon as possible before other depositors access the remaining cash reserves before they do, triggering a cascading crisis that can result in a full-scale bank run.

Money creation

Modern central banking allows multiple banks to practice fractional reserve banking with inter-bank business transactions without risking bankruptcy. The process of fractional-reserve banking has a cumulative effect of money creation by banks, essentially expanding the money supply of the economy.[6]

There are two types of money in a fractional-reserve banking system operating with a central bank:[12][13][14]

- central bank money (money created or adopted by the central bank regardless of its form (precious metals, commodity certificates, banknotes, coins, electronic money loaned to commercial banks, or anything else the central bank chooses as its form of money)

- commercial bank money (demand deposits in the commercial banking system) - sometimes referred to as chequebook money[15]

When a deposit of central bank money is made at a commercial bank, the central bank money is removed from circulation and added to the commercial banks' reserves (it is no longer counted as part of m1 money supply). Simultaneously, an equal amount of new commercial bank money is created in the form of bank deposits. When a loan is made by the commercial bank (which keeps only a fraction of the central bank money as reserves), using the central bank money from the commercial bank's reserves, the m1 money supply expands by the size of the loan.[5] This process is called deposit multiplication.

Example of deposit multiplication

The table below displays how loans are funded and how the money supply is affected. It also shows how central bank money is used to create commercial bank money from an initial deposit of $100 of central bank money. In the example, the initial deposit is lent out 10 times with a fractional-reserve rate of 20% to ultimately create $400 of commercial bank money. Each successive bank involved in this process creates new commercial bank money on a diminishing portion of the original deposit of central bank money. This is because banks only lend out a portion of the central bank money deposited, in order to fulfill reserve requirements and to ensure that they always have enough reserves on hand to meet normal transaction demands.

The process begins when an initial $100 deposit of central bank money is made into Bank A. Bank A takes 20 percent of it, or $20, and sets it aside as reserves, and then loans out the remaining 80 percent, or $80. At this point, the money supply actually totals $180, not $100, because the bank has loaned out $80 of the central bank money, kept $20 of central bank money in reserve (not part of the money supply), and substituted a newly created $100 IOU claim for the depositor that acts equivalently to and can be implicitly redeemed for central bank money (the depositor can transfer it to another account, write a check on it, demand his cash back, etc.). These claims by depositors on banks are termed demand deposits or commercial bank money and are simply recorded in a bank's accounts as a liability (specifically, an IOU to the depositor). From a depositor's perspective, commercial money is equivalent to central bank money – it is impossible to tell the two forms of money apart unless a bank run occurs (at which time everyone wants central bank money).[5]

At this point, Bank A now only has $20 of central bank money on its books. The loan recipient is holding $80 in central bank money, but he soon spends the $80. The receiver of that $80 then deposits it into Bank B. Bank B is now in the same situation as Bank A started with, except it has a deposit of $80 of central bank money instead of $100. Similar to Bank A, Bank B sets aside 20 percent of that $80, or $16, as reserves and lends out the remaining $64, increasing money supply by $64. As the process continues, more commercial bank money is created. To simplify the table, a different bank is used for each deposit. In the real world, the money a bank lends may end up in the same bank so that it then has more money to lend out.

| Individual Bank | Amount Deposited | Lent Out | Reserves |

|---|---|---|---|

| A | 100 | 80 | 20 |

| B | 80 | 64 | 16 |

| C | 64 | 51.20 | 12.80 |

| D | 51.20 | 40.96 | 10.24 |

| E | 40.96 | 32.77 | 8.19 |

| F | 32.77 | 26.21 | 6.55 |

| G | 26.21 | 20.97 | 5.24 |

| H | 20.97 | 16.78 | 4.19 |

| I | 16.78 | 13.42 | 3.36 |

| J | 13.42 | 10.74 | 2.68 |

| K | 10.74 | ||

| Total Reserves: | |||

| 89.26 | |||

| Total Amount of Deposits: | Total Amount Lent Out: | Total Reserves + Last Amount Deposited: | |

| 457.05 | 357.05 | 100 |

Although no new money was physically created in addition to the initial $100 deposit, new commercial bank money is created through loans. The 2 boxes marked in red show the location of the original $100 deposit throughout the entire process. The total reserves plus the last deposit (or last loan, whichever is last) will always equal the original amount, which in this case is $100. As this process continues, more commercial bank money is created. The amounts in each step decrease towards a limit. If a graph is made showing the accumulation of deposits, one can see that the graph is curved and approaches a limit. This limit is the maximum amount of money that can be created with a given reserve rate. When the reserve rate is 20%, as in the example above, the maximum amount of total deposits that can be created is $500 and the maximum increase in the money supply is $400.

For an individual bank, the deposit is considered a liability whereas the loan it gives out and the reserves are considered assets. Deposits will always be equal to loans plus a bank's reserves, since loans and reserves are created from deposits. This is the basis for a bank's balance sheet.

The expansion and contraction of the money supply occurs through this money creation process. When loans are given out, the process moves from the top down and the money supply expands. When currency is withdrawn from the commercial banks, causing loans to be called back, the process moves from the bottom to the top and the money supply contracts.

This table gives an outline of the makeup of money supplies worldwide. Most of the money in any given money supply consists of commercial bank money.[12] The value of commercial bank money is based on the fact that it can be exchanged freely at a bank for central bank money.[12][13]

The actual increase in the money supply through this process may be lower, as (at each step) banks may choose to hold reserves in excess of the statutory minimum, borrowers may let some funds sit idle, and some members of the public may choose to hold cash, and there also may be delays or frictions in the lending process.[19] Government regulations may also be used to limit the money creation process by preventing banks from giving out loans even though the reserve requirements have been fulfilled.[20]

Money multiplier

The most common mechanism used to measure this increase in the money supply is typically called the money multiplier. It calculates the maximum amount of money that an initial deposit can be expanded to with a given reserve ratio.

Formula

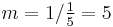

The money multiplier, m, is the inverse of the reserve requirement, R:[21]

Example

For example, with the reserve ratio of 20 percent, this reserve ratio, R, can also be expressed as a fraction:

So then the money multiplier, m, will be calculated as:

This number is multiplied by the initial deposit to show the maximum amount of money it can be expanded to.

The money creation process is also affected by the currency drain ratio (the propensity of the public to hold banknotes rather than deposit them with a commercial bank), and the safety reserve ratio (excess reserves beyond the legal requirement that commercial banks voluntarily hold—usually a small amount). Data for "excess" reserves and vault cash are published regularly by the Federal Reserve in the United States.[22] In practice, the actual money multiplier varies over time, and may be substantially lower than the theoretical maximum.[23]

Reserve requirements

The reserve requirements are intended to prevent banks from:

- generating too much money by making too many loans against the narrow money deposit base;

- having a shortage of cash when large deposits are withdrawn (although the reserve is a legal minimum, it is understood that in a crisis or bank run, reserves may be made available on a temporary basis).

In addition to reserve requirements, there are other required financial ratios that affect the amount of loans that a bank can fund. The capital requirement ratio is perhaps the most important of these other required ratios. When there are no mandatory reserve requirements, the capital requirement ratio acts to prevent an infinite amount of bank lending.

Money supplies around the world

Fractional-reserve banking determines the relationship between the amount of central bank money (currency) in the official money supply statistics and the total money supply. Most of the money in these systems is commercial bank money. Fractional reserve banking involves the issuance and creation of commercial bank money, which increases the money supply through the deposit creation multiplier. The issue of money through the banking system is a mechanism of monetary transmission, which a central bank can influence indirectly by raising or lowering interest rates (although banking regulations may also be adjusted to influence the money supply, depending on the circumstances).

Regulation

Because the nature of fractional-reserve banking involves the possibility of bank runs, central banks have been created throughout the world to address these problems.[4][24]

Central banks

Government controls and bank regulations related to fractional-reserve banking have generally been used to impose restrictive requirements on note issue and deposit taking on the one hand, and to provide relief from bankruptcy and creditor claims, and/or protect creditors with government funds, when banks defaulted on the other hand. Such measures have included:

- Minimum required reserve ratios (RRRs)

- Minimum capital ratios

- Government bond deposit requirements for note issue

- 100% Marginal Reserve requirements for note issue, such as the Bank Charter Act 1844 (UK)

- Sanction on bank defaults and protection from creditors for many months or even years, and

- Central bank support for distressed banks, and government guarantee funds for notes and deposits, both to counteract bank runs and to protect bank creditors.

Liquidity and capital management for a bank

To avoid defaulting on its obligations, the bank must maintain a minimal reserve ratio that it fixes in accordance with, notably, regulations and its liabilities. In practice this means that the bank sets a reserve ratio target and responds when the actual ratio falls below the target. Such response can be, for instance:

- Selling or redeeming other assets, or securitization of illiquid assets,

- Restricting investment in new loans,

- Borrowing funds (whether repayable on demand or at a fixed maturity),

- Issuing additional capital instruments, or

- Reducing dividends.

Because different funding options have different costs, and differ in reliability, banks maintain a stock of low cost and reliable sources of liquidity such as:

- Demand deposits with other banks

- High quality marketable debt securities

- Committed lines of credit with other banks

As with reserves, other sources of liquidity are managed with targets.

The ability of the bank to borrow money reliably and economically is crucial, which is why confidence in the bank's creditworthiness is important to its liquidity. This means that the bank needs to maintain adequate capitalisation and to effectively control its exposures to risk in order to continue its operations. If creditors doubt the bank's assets are worth more than its liabilities, all demand creditors have an incentive to demand payment immediately, a situation known as a run on the bank.

Contemporary bank management methods for liquidity are based on maturity analysis of all the bank's assets and liabilities (off balance sheet exposures may also be included). Assets and liabilities are put into residual contractual maturity buckets such as 'on demand', 'less than 1 month', '2–3 months' etc. These residual contractual maturities may be adjusted to account for expected counter party behaviour such as early loan repayments due to borrowers refinancing and expected renewals of term deposits to give forecast cash flows. This analysis highlights any large future net outflows of cash and enables the bank to respond before they occur. Scenario analysis may also be conducted, depicting scenarios including stress scenarios such as a bank-specific crisis.

Risk and prudential regulation

In a fractional-reserve banking system, in the event of a bank run, the demand depositors and note holders would attempt to withdraw more money than the bank has in reserves, causing the bank to suffer a liquidity crisis and, ultimately, to perhaps default. In the event of a default, the bank would need to liquidate assets and the creditors of the bank would suffer a loss if the proceeds were insufficient to pay its liabilities. Since public deposits are payable on demand, liquidation may require selling assets quickly and potentially in large enough quantities to affect the price of those assets. An otherwise solvent bank (whose assets are worth more than its liabilities) may be made insolvent by a bank run. This problem potentially exists for any corporation with debt or liabilities, but is more critical for banks as they rely upon public deposits (which may be redeemable upon demand).

Although an initial analysis of a bank run and default points to the bank's inability to liquidate or sell assets (i.e. because the fraction of assets not held in the form of liquid reserves are held in less liquid investments such as loans), a more full analysis indicates that depositors will cause a bank run only when they have a genuine fear of loss of capital, and that banks with a strong risk adjusted capital ratio should be able to liquidate assets and obtain other sources of finance to avoid default. For this reason, fractional-reserve banks have every reason to maintain their liquidity, even at the cost of selling assets at heavy discounts and obtaining finance at high cost, during a bank run (to avoid a total loss for the contributors of the bank's capital, the shareholders).

Many governments have enforced or established deposit insurance systems in order to protect depositors from the event of bank defaults and to help maintain public confidence in the fractional-reserve system.

Responses to the problem of financial risk described above include:

- Proponents of prudential regulation, such as minimum capital ratios, minimum reserve ratios, central bank or other regulatory supervision, and compulsory note and deposit insurance, (see Controls on Fractional-Reserve Banking below);

- Proponents of free banking, who believe that banking should be open to free entry and competition, and that the self-interest of debtors, creditors and shareholders should result in effective risk management; and,

- Withdrawal restrictions: some bank accounts may place a limit on daily cash withdrawals and may require a notice period for very large withdrawals. Banking laws in some countries may allow restrictions to be placed on withdrawals under certain circumstances, although these restrictions may rarely, if ever, be used;

- Opponents of fractional reserve banking who insist that notes and demand deposits be 100% reserved.

Example of a bank balance sheet and financial ratios

An example of fractional reserve banking, and the calculation of the reserve ratio is shown in the balance sheet below:

| Example 2: ANZ National Bank Limited Balance Sheet as at 30 September 2007 | |||

|---|---|---|---|

| ASSETS | NZ$m | LIABILITIES | NZ$m |

| Cash | 201 | Demand Deposits | 25482 |

| Balance with Central Bank | 2809 | Term Deposits and other borrowings | 35231 |

| Other Liquid Assets | 1797 | Due to Other Financial Institutions | 3170 |

| Due from other Financial Institutions | 3563 | Derivative financial instruments | 4924 |

| Trading Securities | 1887 | Payables and other liabilities | 1351 |

| Derivative financial instruments | 4771 | Provisions | 165 |

| Available for sale assets | 48 | Bonds and Notes | 14607 |

| Net loans and advances | 87878 | Related Party Funding | 2775 |

| Shares in controlled entities | 206 | [subordinated] Loan Capital | 2062 |

| Current Tax Assets | 112 | Total Liabilities | 99084 |

| Other assets | 1045 | Share Capital | 5943 |

| Deferred Tax Assets | 11 | [revaluation] Reserves | 83 |

| Premises and Equipment | 232 | Retained profits | 2667 |

| Goodwill and other intangibles | 3297 | Total Equity | 8703 |

| Total Assets | 107787 | Total Liabilities plus Net Worth | 107787 |

In this example the cash reserves held by the bank is $3010m ($201m currency + $2809m held at central bank) and the demand liabilities of the bank are $25482m, for a cash reserve ratio of 11.81%.

Other financial ratios

The key financial ratio used to analyze fractional-reserve banks is the cash reserve ratio, which is the ratio of cash reserves to demand deposits. However, other important financial ratios are also used to analyze the bank's liquidity, financial strength, profitability etc.

For example the ANZ National Bank Limited balance sheet above gives the following financial ratios:

- The cash reserve ratio is $3010m/$25482m, i.e. 11.81%.

- The liquid assets reserve ratio is ($201m+$2809m+$1797m)/$25482m, i.e. 18.86%.

- The equity capital ratio is $8703m/107787m, i.e. 8.07%.

- The tangible equity ratio is ($8703m-$3297m)/107787m, i.e. 5.02%

- The total capital ratio is ($8703m+$2062m)/$107787m, i.e. 9.99%.

It is very important how the term 'reserves' is defined for calculating the reserve ratio, as different definitions give different results. Other important financial ratios may require analysis of disclosures in other parts of the bank's financial statements. In particular, for liquidity risk, disclosures are incorporated into a note to the financial statements that provides maturity analysis of the bank's assets and liabilities and an explanation of how the bank manages its liquidity.

How the example bank manages its liquidity

The ANZ National Bank Limited explains its methods as:

Liquidity risk is the risk that the Banking Group will encounter difficulties in meeting commitments associated with its financial liabilities, e.g. overnight deposits, current accounts, and maturing deposits; and future commitments e.g. loan draw-downs and guarantees. The Banking Group manages its exposure to liquidity risk by maintaining sufficient liquid funds to meet its commitments based on historical and forecast cash flow requirements.

The following maturity analysis of assets and liabilities has been prepared on the basis of the remaining period to contractual maturity as at the balance date. The majority of longer term loans and advances are housing loans, which are likely to be repaid earlier than their contractual terms. Deposits include substantial customer deposits that are repayable on demand. However, historical experience has shown such balances provide a stable source of long term funding for the Banking Group. When managing liquidity risks, the Banking Group adjusts this contractual profile for expected customer behaviour.

| Example 2: ANZ National Bank Limited Maturity Analysis of Assets and Liabilities as at 30 September 2007 | ||||||

|---|---|---|---|---|---|---|

| Total carrying value | Less than 3 months | 3–12 months | 1–5 years | Beyond 5 years | No Specified Maturity | |

| Assets | ||||||

| Liquid Assets | 4807 | 4807 | ||||

| Due from other financial institutions | 3563 | 2650 | 440 | 187 | 286 | |

| Derivative Financial Instruments | 4711 | 4711 | ||||

| Assets available for sale | 48 | 33 | 1 | 13 | 1 | |

| Net loans and advances | 87878 | 9276 | 9906 | 24142 | 44905 | |

| Other Assets | 4903 | 970 | 179 | 3754 | ||

| Total Assets | 107787 | 18394 | 10922 | 25013 | 45343 | 8115 |

| Liabilities | ||||||

| Due to other financial institutions | 3170 | 2356 | 405 | 32 | 377 | |

| Deposits and other borrowings | 70030 | 53059 | 14726 | 2245 | ||

| Derivative financial instruments | 4932 | 4932 | ||||

| Other liabilities | 1516 | 1315 | 96 | 32 | 60 | 13 |

| Bonds and notes | 14607 | 672 | 4341 | 9594 | ||

| Related party funding | 2275 | 2275 | ||||

| Loan capital | 2062 | 100 | 1653 | 309 | ||

| Total liabilities | 99084 | 60177 | 19668 | 13556 | 746 | 4937 |

| Net liquidity gap | 8703 | (41783) | (8746) | 11457 | 44597 | 3178 |

| Net liquidity gap - cumulative | 8703 | (41783) | (50529) | (39072) | 5525 | 8703 |

Criticism

The primary criticisms relate to the potential fragility of bank liquidity in a fractional reserve banking environment, the financial risk of bank runs that depositors bear when depositing money with banks, and the impact that demand deposits have on the stock of money, and on inflation (that is, the implicit expansion of the money supply and its associated impact on prices and the exchange rate). An alternative to fractional reserve banking is full-reserve banking.[25] With full-reserve banking, some monetary reformers, such as Stephen Zarlenga of the American Monetary Institute, support the concurrent issuance of debt-free fiat currency from the Treasury, while others such as Congressman Ron Paul and the Ludwig von Mises Institute call for a commodity currency as existed under the gold standard.[26][27][28]

Exacerbation of the business cycle

Some Austrian School economists claim that fractional-reserve banking, by expanding the money supply, will lower the interest rates compared to a hypothetical full-reserve banking system. They argue that this will affect the role of the interest rate as the price of investment capital, guiding investment decisions. One of the proponents of aspects of the business cycle theory, Friedrich von Hayek, shared in the Nobel Memorial Prize in Economic Sciences for 1974.[29] Hayek accepted that bank credit and fractional reserve banking — even if they contributed to business cycles — were necessary as "the price we pay for a speed of development exceeding" that which would otherwise be possible, and that "financial institutions have never been prohibited from holding fractional reserves."[30]

A few Austrian School economists, such as Pascal Salin, also suggest that a full-reserve banking system should not be enforced legally, and dispute Murray Rothbard's characterization of fractional-reserve banking as a simple form of recursive embezzlement, and rather advocate the abolition of central banking, and suggest that free banking replace the current system. Austrian monetary theorist George Selgin has argued: "Those self-styled Austrian economists, mostly followers of Murray Rothbard, who insist on fractional-reserve banking's fraudulent nature or inherent instability are, frankly, making poor arguments. I don't think the evidence supports their view, and that they overlook overwhelming proof of the benefits that fractional reserve banking has brought in the way of economic development by fostering investment."[31]

But many Austrians, such as Jeffrey Herbener, believe Selgin's view of fractional-reserve banking is at odds with that of Ludwig Von Mises: "George Selgin and Lawrence White have sought to tie their modern free banking school to the views of Ludwig von Mises... Whatever the validity of their own views on the gold standard and fractional-reserve free banking, their assessments of Mises's positions on these issues are dubious."[32]

Effects of an increased money supply

Fractional reserve banking involves the creation of money by commercial banks, increasing the money supply of a country. According to the quantity theory of money, this larger money supply leads to more money 'chasing' the same amount of goods, which leads to a higher price level.[33] Austrian economists state that this expansion of the broad money supply (demand deposits and notes) caused by fractional reserve banking is a cause of inflation.[34] The Credit Theory of Money, as espoused by Southampton University economist Richard Werner, says that credit creation by banks does not necessarily result in inflation.[35] This depends on the use of newly created credit. Disaggregating credit into credit used for GDP and non-GDP transactions, Werner further distinguishes between 'productive' and 'unproductive' credit creation. The latter always results in inflation (in the case of GDP transactions, consumer price inflation; in the case of non-GDP transactions, asset price inflation or unsustainable asset bubbles which will result in a banking crisis). The former will always increase real growth, even when all resources are fully employed, provided that there is new technology that has not yet been implemented (as productive credit creation serves to implement it).

See also

- Islamic banking

- Narrow banking

- Open Market Operations

- Seignorage

- Usury

References

- ↑ The Bank Credit Analysis Handbook: A Guide for Analysts, Bankers and Investors by Jonathan Golin. Publisher: John Wiley & Sons (August 10, 2001). ISBN 0471842176 ISBN 978-0471842170

- ↑ Bankintroductions.com - Economic Definitions

- ↑ 3.0 3.1 United States. Congress. House. Banking and Currency Committee. (1964). Money facts; 169 questions and answers on money- a supplement to A Primer on Money, with index, Subcommittee on Domestic Finance ... 1964.. Washington D.C.. http://books.google.com/?id=9DlDs-o0arUC&q=goldsmiths.

- ↑ 4.0 4.1 The Federal Reserve in Plain English - An easy-to-read guide to the structure and functions of the Federal Reserve System. See page 5 of the document for the purposes and functions: http://www.frbsf.org/publications/education/plainenglish/index.html

- ↑ 5.0 5.1 5.2 5.3 Mankiw, N. Gregory (2002), "Chapter 18: Money Supply and Money Demand", Macroeconomics (5th ed.), Worth, pp. 482–489

- ↑ 6.0 6.1 Page 57 of 'The FED today', a publication on an educational site affiliated with the Federal Reserve Bank of Kansas City) designed to educate people on the history and purpose of the United States Federal Reserve system. http://www.federalreserveeducation.org/fed101/fedtoday/FedTodayAll.pdf

- ↑ Abel, Andrew; Bernanke, Ben (2005), "7", Macroeconomics (5th ed.), Pearson, pp. 266–269

- ↑ Whelan, Karl (2009-01-29). "International Monetary Economics: Banks and Financial Intermediation" (PDF). School of Economics, University College Dublin. http://www.karlwhelan.com/Teaching/International%20Monetary/part3.pdf. Retrieved 2009-10-29.

- ↑ Mankiw, N. Gregory (2002), "9", Macroeconomics (5th ed.), Worth, pp. 238–255

- ↑ Caplan, Bryan (2009-10-28). "Additive Shocks". EconLog. Library of Economics and Liberty. http://econlog.econlib.org/archives/2009/10/additive_shocks.html. Retrieved 2009-10-29.

- ↑ Committee on Finance and Industry 1931 (Macmillan Report) on bankers desire to complicate banking issues."The economic experts have evolved a highly technical vocabulary of their own and in their zeal for precision are distrustful, if not derisive of any attempts to popularize their science."

- ↑ 12.0 12.1 12.2 12.3 Bank for International Settlements - The Role of Central Bank Money in Payment Systems. See page 9, titled, "The coexistence of central and commercial bank monies: multiple issuers, one currency": http://www.bis.org/publ/cpss55.pdf A quick quote in reference to the 2 different types of money is listed on page 3. It is the first sentence of the document:

- "Contemporary monetary systems are based on the mutually reinforcing roles of central bank money and commercial bank monies."

- ↑ 13.0 13.1 European Central Bank - Domestic payments in Euroland: commercial and central bank money: http://www.ecb.int/press/key/date/2000/html/sp001109_2.en.html One quote from the article referencing the two types of money:

- "At the beginning of the 20th almost the totality of retail payments were made in central bank money. Over time, this monopoly came to be shared with commercial banks, when deposits and their transfer via cheques and giros became widely accepted. Banknotes and commercial bank money became fully interchangeable payment media that customers could use according to their needs. While transaction costs in commercial bank money were shrinking, cashless payment instruments became increasingly used, at the expense of banknotes"

- ↑ Macmillan report 1931 account of how fractional banking works http://books.google.ca/books?hl=en&id=EkUTaZofJYEC&dq=British+Parliamentary+reports+on+international+finance&printsec=frontcover&source=web&ots=kHxssmPNow&sig=UyopnsiJSHwk152davCIyQAMVdw&sa=X&oi=book_result&resnum=1&ct=result#PPA34,M1

- ↑ Chicago Fed - Our Central Bank: http://www.chicagofed.org/consumer_information/the_fed_our_central_bank.cfm

- the reference is found in the "Money Manager" section:

- "the Fed works to control money at its source by affecting the ability of financial institutions to "create" chequebook money through loans or investments. The control lever that the Fed uses in this process is the "reserves" that banks and thrifts must hold."

- the reference is found in the "Money Manager" section:

- ↑ Table created with the OpenOffice.org Calc spreadsheet program using data and information from the references listed.

- ↑ Federal Reserve Education - How does the Fed Create Money? http://www.federalreserveeducation.org/fed101_html/policy/money_print.htm

- See the link to "The Principle of Multiple Deposit Creation" pdf document towards bottom of page.

- ↑ An explanation of how it works from the New York Regional Reserve Bank of the US Federal Reserve system. Scroll down to the "Reserve Requirements and Money Creation" section. Here is what it says:

- "Reserve requirements affect the potential of the banking system to create transaction deposits. If the reserve requirement is 10%, for example, a bank that receives a $100 deposit may lend out $90 of that deposit. If the borrower then writes a check to someone who deposits the $90, the bank receiving that deposit can lend out $81. As the process continues, the banking system can expand the initial deposit of $100 into a maximum of $1,000 of money ($100+$90+81+$72.90+...=$1,000). In contrast, with a 20% reserve requirement, the banking system would be able to expand the initial $100 deposit into a maximum of $500 ($100+$80+$64+$51.20+...=$500). Thus, higher reserve requirements should result in reduced money creation and, in turn, in reduced economic activity."

- ↑ http://books.google.com/books?id=I-49pxHxMh8C&pg=PA303&dq=deposit+reserves&lr=&sig=hMQtESrWP6IBRYiiaZgKwIoDWVk#PPA295,M1 William MacEachern, Macroeconomics: A Contemporary Introduction, p. 295

- ↑ ebook: The Federal Reserve - Purposes and Functions:http://www.federalreserve.gov/pf/pf.htm

- see pages 13 and 14 of the pdf version for information on government regulations and supervision over banks

- ↑ http://www.mhhe.com/economics/mcconnell15e/graphics/mcconnell15eco/common/dothemath/moneymultiplier.html

- ↑ http://www.federalreserve.gov/releases/h3/Current/ Federal Reserve Board, "AGGREGATE RESERVES OF DEPOSITORY INSTITUTIONS AND THE MONETARY BASE" (Updated weekly).

- ↑ http://books.google.com/books?id=FdrbugYfKNwC&pg=PA169&lpg=PA169&dq=united+states+money+multiplier&source=web&ots=C_Hw1u82xe&sig=m7g0bMz167DijFsOCbn5f4aWAOU#PPA170,M1 Bruce Champ & Scott Freeman, Modeling Monetary Economies, p. 170 (Figure 9.1).

- ↑ Reserve Bank of India - Report on Currency and Finance 2004-05 (See page 71 of the full report or just download the section Functional Evolution of Central Banking): http://www.rbi.org.in/scripts/AnnualPublications.aspx?head=Report%20on%20Currency%20and%20Finance&fromdate=03/17/06&todate=03/19/06

- The monopoly power to issue currency is delegated to a central bank in full or sometimes in part. The practice regarding the currency issue is governed more by convention than by any particular theory. It is well known that the basic concept of currency evolved in order to facilitate exchange. The primitive currency note was in reality a promissory note to pay back to its bearer the original precious metals. With greater acceptability of these promissory notes, these began to move across the country and the banks that issued the promissory notes soon learnt that they could issue more receipts than the gold reserves held by them. This led to the evolution of the fractional reserve system. It also led to repeated bank failures and brought forth the need to have an independent authority to act as lender-of-the-last-resort. Even after the emergence of central banks, the concerned governments continued to decide asset backing for issue of coins and notes. The asset backing took various forms including gold coins, bullion, foreign exchange reserves and foreign securities. With the emergence of a fractional reserve system, this reserve backing (gold, currency assets, etc.) came down to a fraction of total currency put in circulation.

- ↑ Murray Rothbard, The Mystery of Banking

- ↑ Stephen A. Zarlenga, The Lost Science of Money AMI (2002)

- ↑ Paper Money and Tyranny, Ron Paul

- ↑ Fiat Paper Money, Ron Paul.

- ↑ The Prize in Economics 1974 - Press Release

- ↑ http://mises.org/journals/rae/pdf/RAE9_1_3.pdf Walter Block and Kenneth A. Garschina, "Hayek, Business Cycles and Fractional Reserve Banking: Continuing the De-Homogenization Process", Review of Austrian Economics, 1996.

- ↑ Slivinski, Stephen. "Interview: George Selgin". The Federal Reserve Bank of Richmond. http://www.richmondfed.org/publications/research/region_focus/2009/winter/full_interview.cfm. Retrieved 2009-10-29.

- ↑ http://mises.org/journals/qjae/pdf/qjae5_1_4.pdf

- ↑ Charles T. Hatch, Inflationary Deception

- ↑ Ludwig von Mises, The Theory of Money and Credit, ISBN 0-913966-70-3 [1] See also: Jesus Huerta de Soto, Money, Bank Credit, and Economic Cycles, ISBN 0-945466-39-4 [2]

- ↑ Richard A. Werner (2005), New Paradigm in Monetary Economics, Basingstoke: Palgrave Macmillan

Further reading

- Crick, W.F. (1927), The genesis of bank deposits, Economica, vol 7, 1927, pp 191–202.

- Friedman, Milton (1960), A Program for Monetary Stability, New York, Fordham University Press.

- Meigs, A.J. (1962), Free reserves and the money supply, Chicago, University of Chicago, 1962.

- Philips, C.A. (1921), Bank Credit, New York, Macmillan, chapters 1-4, 1921,

- Thomson, P. (1956), Variations on a theme by Philips, American Economic Review vol 46, December 1956, pp. 965–970.

- Federalreserveeducation.org - The Principle of Multiple Deposit Creation

- Reserve Requirements - Fedpoints - Federal Reserve Bank of New York

- Bank for International Settlements - The Role of Central Bank Money in Payment Systems

External links

- Narrow banking

- Modern Money Mechanics Federal Reserve Document explaining how money is created.